The global financial crisis of 2008 marked the beginning of almost 15 years of expansionary monetary policy in Europe, the United States, and other developed countries, commonly referred to as the Low for Long era.

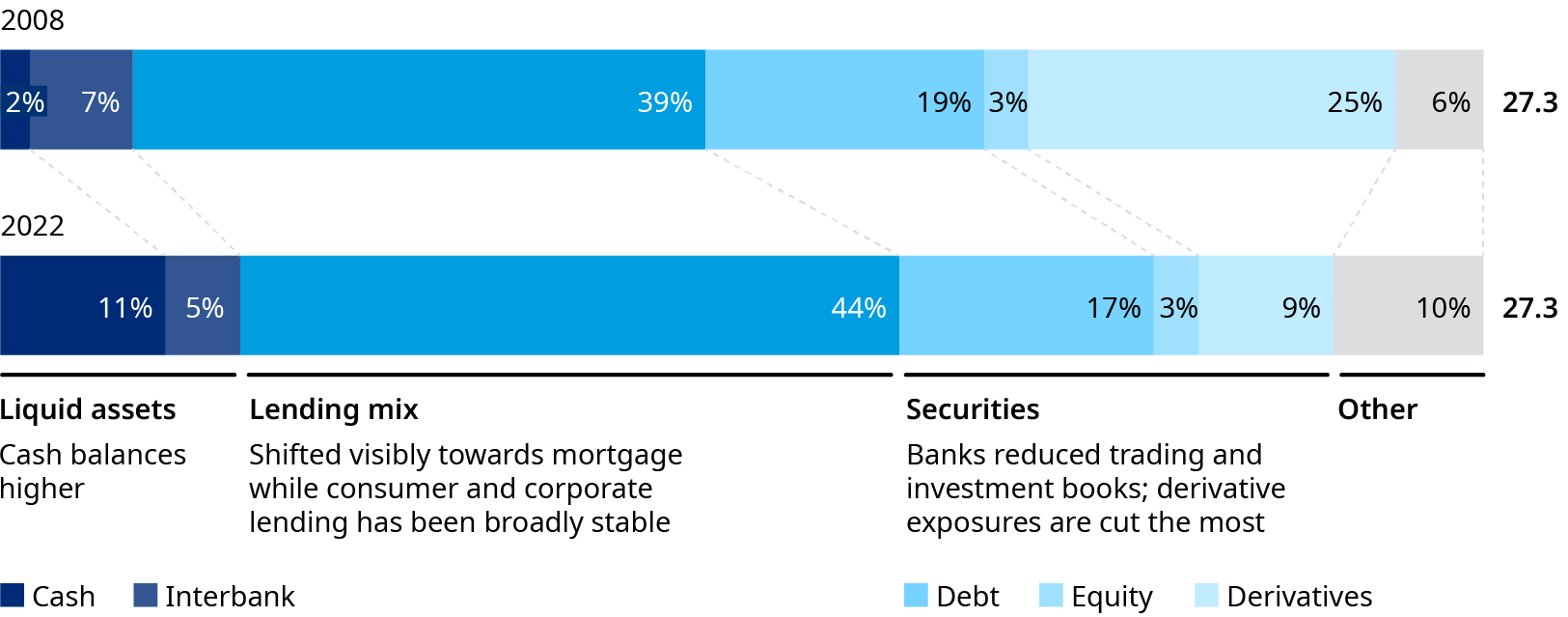

The period was marked by a significant transformation of Europe’s financial system, particularly in leverage and risk-taking dynamics. The role of European banks in funding the real economy diminished as they deleveraged and simplified their balance-sheet structure under more stringent regulations. Concurrently, non-bank financial institutions (NBFI) and their investors in search for yield assumed a more important role as financers, gaining market share in lending from banks. Governments also took advantage of low rates to fund reforms, social expenditure, and economic stimulus.

Exploring the New Monetary Order and Low for Long implications

The Low for Long era came to an abrupt end in 2022 as central banks swiftly raised interest rates and started to unwind balance sheets in response to rampant inflation. We have labeled the resulting environment, characterized by high inflation, substantially enlarged balance sheets, and high public debt as the New Monetary Order (NMO). The New Monetary Order is reversing more than a decade of developments, causing short-term blowouts and raising questions about long-term sustainability of business models for financial institutions, non-financial corporations, and sovereigns.

Navigating economic realities in the New Monetary Order

The nature and extent of vulnerabilities may still not be fully known and understood. Moreover, geopolitical tensions, technological disruptions, climate change, and aging populations add to substantial funding pressures for already indebted European economies, with recent rate hikes having reignited concerns about debt sustainability for both corporates and governments. Financial institutions and non-financial corporates will need to clarify impacts and revamp business models, with support from the public sector, to successfully navigate the new monetary and economic realities.

This paper focuses on the European experience. While many of these themes were present globally, experiences varied by country and region. As a result, we are releasing separate reports providing perspectives on the New Monetary Order for the United States, Europe, Asia, and Australia.